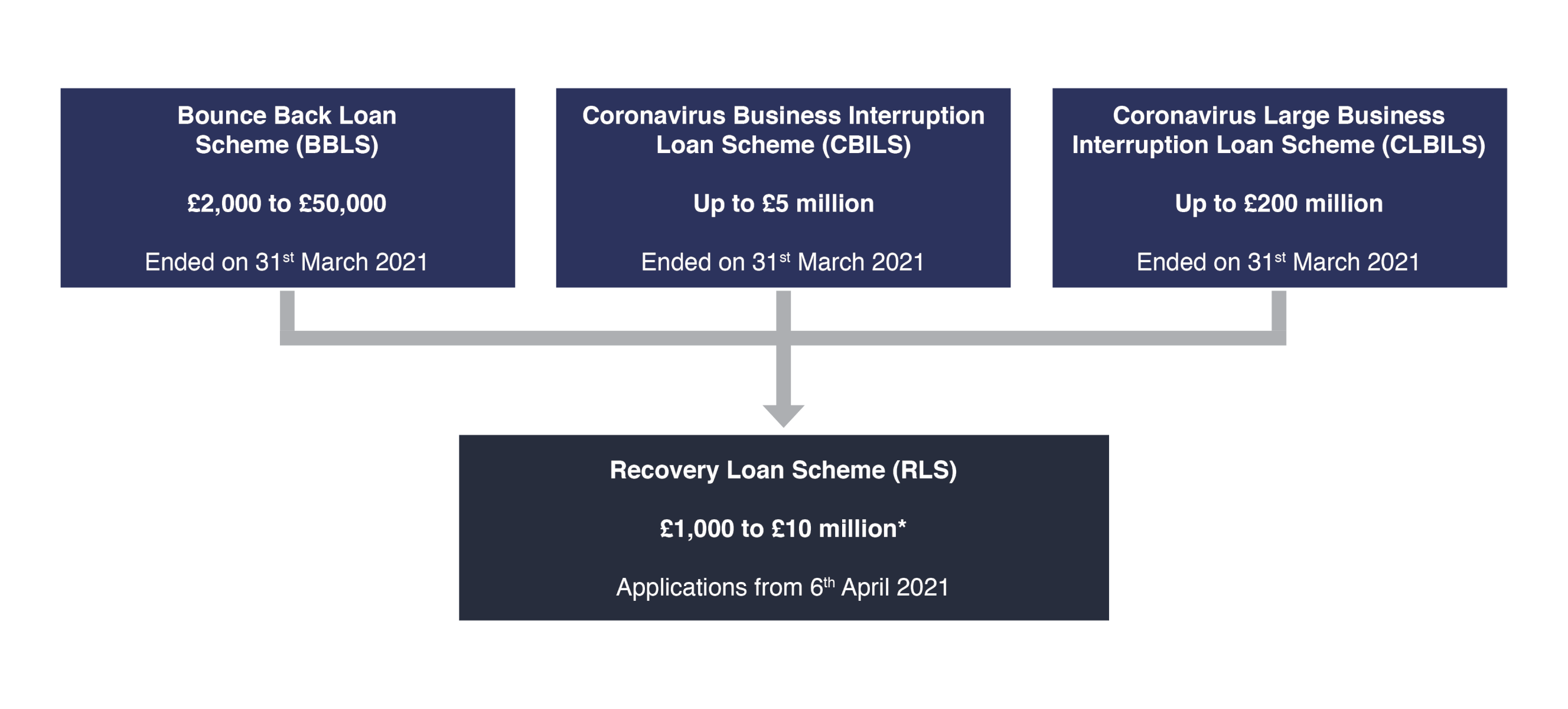

RLS – Recovery Loan Scheme

The Government has announced that a new lending scheme which they are calling the Recovery Loan Scheme will launch on 6 April 2021 and is scheduled to run until 31 December 2021, subject to review.

The new scheme is designed to help businesses affected by Covid-19 recover and grow post-pandemic and can be used for any legitimate business purpose, including managing cash flow, investment, and growth.

It is designed to appeal to businesses that can afford to take out additional debt finance for these purposes.

What is the Recovery Loan Scheme

As part of HM Treasury’s efforts to Build Back Better, British Business Bank has again been tasked with sustaining the roll-out of critical business funding. The consolidation of existing loan arrangements into a single Recovery Loan Scheme (RLS) signals a desire to release many enterprises from long-term state dependency. The previous schemes had defined criteria around the size of the business applying, along with different amounts of borrowing available depending on its scale. The RLS will be a single offering for businesses of all sizes and life stages.

The new scheme will support borrowing of up to £10 million for individual businesses, and up to £30 million across a group, and can be used for business purposes including managing cash flow, investment, and growth. It is designed to appeal to businesses that can afford to take out additional finance, providing them with continued support as they steer a path towards a sustainable recovery. Like CBILS – the Recovery Loan Scheme’s predecessor – borrowers can choose from term loans, overdrafts, asset finance, and invoice finance, and we expect there will be a large number of participating lenders.

Amalgamating the three COVID loan initiatives into a single scheme

At a glance – CBILS and RLS comparison

| Feature | CBILS | RLS |

|---|---|---|

| Loan amount | £50,000 to £5 million | Up to £10 million |

| Term | Up to six years | Up to six years |

| Government pays first 12 months’ interest | Yes | No |

| Government pays upfront lender fees | Yes | No |

| 80% Government lender guarantee | Yes | No |

| Personal Guarantee | Not permitted on loans up to £250,000 | Not permitted on loans up to £250,000 |

| Minimum trading history requirements | One to two years | No minimum |

| Minimum annual turnover | No minimum | No minimum |

Key Features

⦁ Up to £10m facility per business

Turnover limit

Wide range of products

Term length

Interest and fees to be paid by the business from the outset

Access to multiple schemes

Credit checks for all applicants

In more detail – CBILS and RLS comparison

| Feature | CBILS | RLS |

|---|---|---|

| Scheme duration | The initial six-month duration was extended three times – the scheme closed on the 31st March 2021 | Initially, the scheme has a nine-month duration (6th April to 31st December 2021). There will likely be a review in the autumn to determine if/how the scheme will be extended or amended |

| Facilities |

|

|

| Facility size |

|

|

| Borrower size | SMEs only (turnover less than £45 million) | No turnover limit |

| Maximum amount per borrower | Maximum amount per borrower limited to the lesser of:

|

Maximum amount per borrower limited to the lesser of:

|

| Lender guarantee coverage | 80% | 80% |

| Business Interruption Payment (BIP) | First year’s interest and fees paid by the Government | n/a |

| Facility tenure | Minimum three months, maximum of:

|

Minimum three months, maximum of:

|

| Additionality | n/a | The lender can only provide a facility if:

|

| Refinancing | 20% of total portfolio, not including BBLS or smaller scheme facilities | 20% of the total portfolio, not including refinancing a

CLBILS, CBILS or BBLS facility. Refinancing will only consist of the actual internal debt being refinanced, as opposed to the whole facility, which was the case under CBILS |

| Use of multiple schemes | CBILS borrowers could not use BBLS, unless the new scheme facility refinances the whole of the existing facility | Borrower may have other facilities supported by BBLS or CBILS/CLBILS, and may not be required to refinance them |

| Subsidy regime | EU Temporary Framework for state aid | Domestic subsidy regime, except for those businesses captured by the ‘Northern Ireland Protocol’ accompanying the UK-EU trade agreement – for whom EU state aid rules will still apply |

| Guarantee level (Invoice finance variant only) | Maximum of 30% of Gross Book Debt as a Top-Up Facility and established as a percentage of Gross Book Debt | Lender chooses whether the guarantee covers all or part of the facility limit. This is a £ guarantee (not a %). Once established, it remains a fixed £ value for the tenure of the guarantee. The guarantee must not exceed the facility limit |

| Facility limit (Invoice finance variant only) | Maximum of 30% of Gross Book Debt | Up to the facility limit. The facility limit can be increased to accommodate some extraordinary events but cannot include inter-company debt, aged debtors, and disputed debt |

Who is eligible?

As the Recovery Loan Scheme is intended to aid the recovery of all UK businesses, across all sectors, recover and grow this year.

It has to be expected that the pandemic and measures taken by the Government will have had a negative impact on businesses. It is anticipated that where poorer financial performance is due to Covid-19 that accredited lenders will overlook what might otherwise be normal concerns about the short to medium-term performance of the applying business.

But it is inevitable that the approach taken by accredited lenders will vary subject to their respective credit policies and criteria. The new scheme will almost certainly provide accredited lenders enough flexibility to impose their own requirements, particularly as they aim to mitigate and balance risk across their portfolios.

Looking for a recovery loan scheme loan?

As with the CBILS scheme, the lending will be provided by accredited lenders and will encompass loans, asset finance, invoice finance, overdraft, and property lending.

If you are looking to take out a loan using the Recovery Loan Scheme and need some advice, please don’t hesitate to contact us.