Revolving Credit Facility for businesses

A revolving credit facility (RCF) is a flexible working capital solution, similar to a standard bank overdraft,by which you can draw down cash, repay when you are able and draw down again.The flexibility of the facility means that it is a fantastic option for fuelling growth strategies, delivering acquisitions or just strengthening working capital.

Download our product guide for a comprehensive and easy to read guide on this revolving facility for businesses.

PRODUCT AT A GLANCE

Facility type

Revolving Credit Facility – a flexible solution to cashflow for your business

Advance %

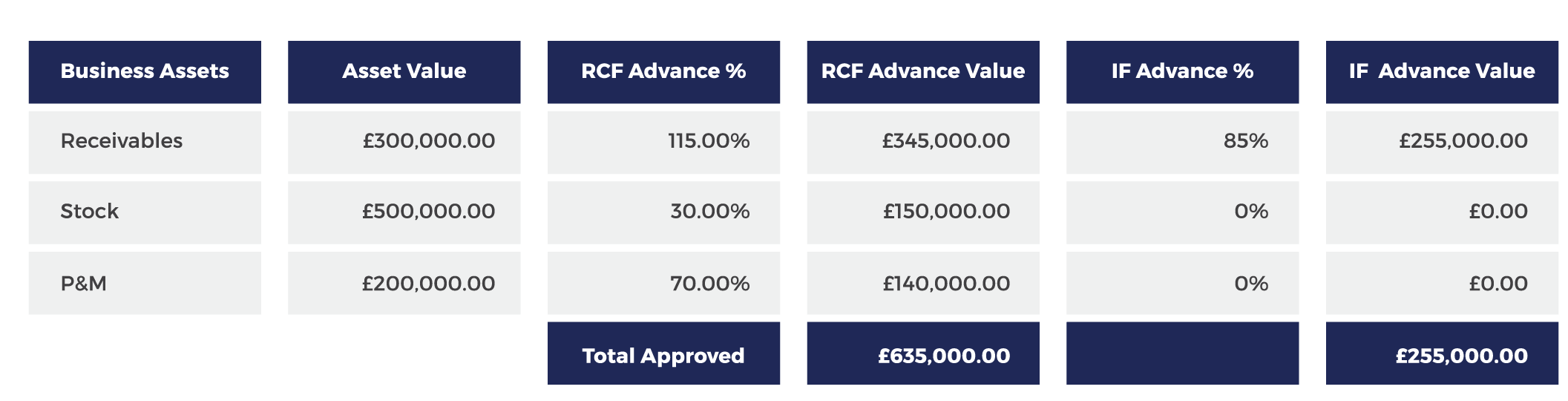

Up to 120% against receivables, 30% against stock and 70% against P&M

Cost

8-12% per annum charged only against usage of the facility

Eligibility

Proven business model, Min turnover of £500,000, May be loss-making (if profitability is forecast against reasonable growth assumptions), B2B – excluding construction sector

Assets leveraged

Receivables, Stock and P&M

Key benefits

Draw down, repay and re draw when you like; simple fair fee structure; maximise cashflow, no debtor contact

BENEFITS OF A REVOLVING CREDIT FACILITY

Flexible drawdowns

Use the facility and draw down cash when you need it and repay when you are able.

Generate more cash

The facility can generate cashflow against multiple asset classes including up to 120% of accounts receivables, up to 30% against Stock and up to 70%

against P&M.

Support growth

The facility has a max borrowing limit of £20m and is available in multiple currencies and across multiple jurisdictions. This is all available in the one single

facility.

Simple fee structures

Only pay for what you use and for how long you use it for. Rates are between 8% to 12% a year and only on drawn funds.

Simple management

No need for interaction with your customers. There is no need to verify invoices with customers due to how the facility is administered.

Significant cashflow support

Access up to 150% more funding than with traditional invoice finance facilities.

REVOLVING CREDIT FACILITY

VS

INVOICE FINANCE

The Revolving Credit Facility is more akin to an Asset Based Lending Facility as it is able to leverage your entire balance sheet whereas an invoice finance facility leverages the accounts receivables only. This means that the Revolving Credit Facility will generate more cash than traditional working capital facilities.

The table below shows the difference between a revolving credit facility and invoice financing and how much more the Revolving Credit Facility can generate for your business.

FAQ's

What is a revolving credit facility?

What can a revolving credit facility lend against?

How does a revolving credit facility work?

What can a revolving credit facility be used for?

Some companies may use a revolving credit facility regularly, whereas others may use it only a handful of times during the agreed term: the frequency depends on each firm’s business model and its cash flow needs.

What is the difference between a revolving credit facility and invoice finance?

What is the difference between a revolving credit facility and a term loan?

1. The advance rate, or how much cash a facility can leverage, of a revolving credit facility is very often much higher than what would be available from a traditional invoice finance facility, which in general is capped at 90% of accounts receivables. The revolving credit facility is also able to generate cash from more of the balance sheet that just the accounts receivable.

2. The cost of the revolving credit facility is simpler to understand. Interest is just charged against the outstanding balance (ie the facility funds in use), as opposed to paying a fixed monthly fee whether you are borrowing any money or not.

What are the eligibility criteria for a revolving credit facility?

Connect With Us

Do you have questions? Contact us today, we’re here to help.